Weight Indicator,Scale Indicator,Stainless Steel Indicator,Weighing Indicators Changzhou Weibo Weighing Equipment CO .,LTD , https://www.webowtscale.com In August, due to the fall in fixed asset investment and the growth of manufacturing industry, the domestic steel market continued to experience weak demand, and steel prices continued to fall. As steel production and social inventories have declined, the country has further introduced steady growth measures. It is expected that steel prices in the market will stabilize in the later period, but it is difficult to reverse the market conditions where supply exceeds demand.

In August, due to the fall in fixed asset investment and the growth of manufacturing industry, the domestic steel market continued to experience weak demand, and steel prices continued to fall. As steel production and social inventories have declined, the country has further introduced steady growth measures. It is expected that steel prices in the market will stabilize in the later period, but it is difficult to reverse the market conditions where supply exceeds demand.

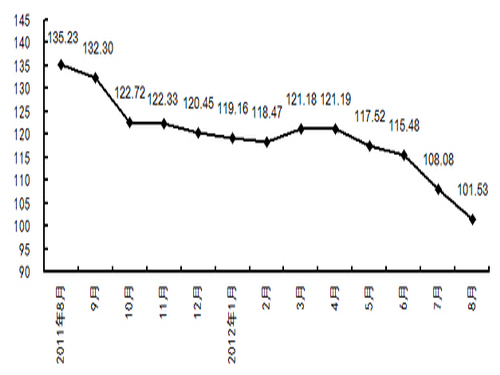

1. In the domestic market, steel prices continued to decline, with a slight decrease compared to the previous month. At the end of August, the CSPI steel comprehensive price index of the China Iron and Steel Association was 101.53 points, a decrease of 6.55 points from the previous month, and a decrease of 6.06%, 0.35 percentage points less than the previous month's decline. ; Compared with the same period of last year, it decreased by 33.70 points, a decrease of 24.92%.

1. The long products and sheet metals indices continued to decline. At the end of August, the CSPI longevity index was 105.02 points, a 6.11 point decrease from the previous period, a decrease of 5.50%, a decrease of 1.54 percentage points from the previous month's decline; the sheet index fell below 100 points, at 98.58 points. In point, it was down by 6.99 points, a decrease of 6.62%, which was a decrease of 0.10 percentage points from the previous month's decline. Compared with the same period of last year, the long products index decreased by 38.35 points, a decrease of 26.75%; the sheet index decreased by 31.77 points, a decrease of 24.37%. .

2. The prices of major steel products continued to decline At the end of August, prices of the eight steel products monitored by the China Iron and Steel Association continued to decline. Among them, the plate and hot-rolled coils fell by a large margin and fell by 7.25% and 6.94% respectively over the previous quarter; the prices of high-grade, rebar and angle steel decreased by 4.91%, 5.32% and 5.59% respectively; the prices of cold-rolled sheet and galvanized sheet The chain ratios decreased by 3.92% and 3.77% respectively. The price of hot-rolled seamless pipes decreased by 5.34%.

3. Steel prices continued to decline from week to week In August, steel prices in the domestic market continued to decline, with the decline in the first two weeks being relatively small and increasing in the latter two weeks. By the first week of September, the composite index of steel prices had dropped to 99.24 points, which had dropped for the 21st consecutive week since the second week of April.

Second, the domestic market analysis of steel price changes in August, the country's crude steel output fell slightly for the second consecutive month, but by the impact of fixed assets investment and the continued slowdown in manufacturing growth and other factors, the domestic steel market is still presented as oversupply Situation, steel prices continue to fall.

1. The growth rate of the steel industry continues to fall and the demand for steel products remains weak. According to the data from the National Bureau of Statistics, from January to August, the national fixed asset investment (excluding rural households) increased by 20.2% year-on-year, and the growth rate dropped 4.8 percentage points from the same period of last year. The national investment in real estate development increased by 15.6% year-on-year, and the growth rate fell by 17.6% from the same period of last year. In August, the value-added of industrial enterprises above designated size increased by 8.9% year-on-year, 0.3% lower than that in July, and the fourth consecutive monthly growth rate. Fall back. Among them, the growth rates of general-purpose equipment manufacturing, electrical machinery and equipment manufacturing, and electronic equipment manufacturing continued to fall; the total retail sales of consumer goods increased by 13.2% year-on-year, a deceleration of 3.8 percentage points from the same period of last year; The value increased by 0.2% year-on-year, of which exports grew by 2.7%, which were significantly lower than the growth rate of the same period of the previous year by 26.9 and 21.8 percentage points respectively; China's manufacturing PMI was 49.2%, down by 0.9% from the previous month, and was the fourth month in a row. Fall back. The new orders and new export orders index were 48.7% and 46.6%, respectively, still below the 50% cut-off point. Affected steel industry continued to decline in the growth rate, the domestic steel market demand growth is weak.

2. The output of steel products declined slightly, and the total supply of resources still exceeded supply. According to data from the National Bureau of Statistics, the country’s crude steel production in August was 58.70 million tons, a year-on-year decrease of 1.7%; the average daily output of crude steel was 1,938,600 tons, a drop of 96,400 tons. For the second month in a row, the decline rate was 4.84%. According to customs statistics, in August, China exported 4.24 million tons of steel, a decrease of 80,000 tons, a decrease of 1.85%; imported steel 1.2 million tons, an increase of 40,000 tons, an increase of 3.45%; imported steel billet 30,000 tons, unchanged from the previous month. The total billet equivalent to 3.2 million tons of crude steel exports, a decrease of 130,000 tons. Based on the above data, the daily average domestic crude steel supply in August was 1,790,300 tons, a decrease of 92,300 tons, a decrease of 4.90%. Although the supply of steel resources has declined, the oversupply in the domestic market has not significantly improved.

3. The decrease in stocks of steel products has increased, which is still higher than the level at the beginning of the year to the end of August. The social inventory of 26 major steel markets and five kinds of steel products (middle plates, cold rolled sheets, hot rolled sheets, wire rods, and rebars) is 14.33 million tons, a decrease of 1.05 million tons from the end of last month, a decrease of 6.81%, an increase of 5.74 percentage points over the previous month, the sixth consecutive month of decline; but compared with the beginning of the year and the same period last year, inventory still increased by 1.43 million Tons and 500,000 tons, an increase of 11.10% and 3.59% respectively.

In terms of sub-categories, the inventory of wire rods and rebars decreased significantly, falling by 33.96% and 10.81% respectively; the medium- and cold-rolled sheet warehouses continued to decline by 1.06% and 1.46% respectively; the stock of hot-rolled coils continued to rise slightly. The increase was 1.27%.

3. The price of steel in the international market continued to decline, and the decline rate also narrowed. At the end of August, the CRU International Steel Composite Price Index fell to 177.2 points, a decrease of 2.7 points or a decrease of 1.5%, which was a decrease of 1.8% from the previous month; the same period last year In comparison, the overall international steel price index fell by 25.2 points, a decrease of 12.5%.

1. The prices of long products and sheets continued to decline, and the decline of sheet metal was lower than that of long products. At the end of August, the CRU international long steel price index was 197.1 points, a decrease of 6.8 points from the previous month, a decrease of 3.3%, and a decrease of 1.7 percentage points from the previous month; The index was 167.4 points, a decrease of 0.6 points from the previous quarter and a decrease of 0.4%, which was a narrowing of 1.9 percentage points from the previous month. Compared with the same period of last year, the long products index decreased by 37.8 points, a decrease of 16.1%; the sheet index decreased by 18.9 points, a decrease of 10.1%.

2. The steel prices in the North American market rebounded. The European and Asian markets continued to decline. (1) North American market At the end of August, the CRU North American steel price index was 170.1 points, which was a 5.2 point increase or 3.2% increase from the previous quarter. The US market demand situation has improved. In August, the non-agricultural unemployment rate in the United States was 8.1%, a decrease of 0.2% from the previous month; the consumer confidence index (University of Michigan) was 74.3 points, up 2.0 points from the previous month; the manufacturing PMI fell. To 49.6%, a slight decrease of 0.2% from the previous month; the total number of steel import license applications rose by 0.3%. Among them, heavy structural steel, steel bars, hot-rolled bars, medium-thick plates, cold-rolled steel plates, and tin-plated plates increased more; at the end of August, U.S. crude steel capacity utilization rate was 75.4%, which was a 0.7% increase from the previous month. This month, the prices of long products and plates in the Midwestern United States continued to decline, and the prices of thin plates increased.

(2) European market At the end of August, the CRU European steel price index was 175.1 points, down 1.9 points month-on-month, a decrease of 1.1%. The economic downturn in the European Union continued. In August, the economic prosperity index of the Eurozone and the European Union fell to 86.1 points and 87 points, respectively. It has been falling for 5 consecutive months, the lowest level since 2009; the eurozone consumer confidence index and The industrial prosperity index fell 3.1 points and 0.3 points respectively from the previous month; the manufacturing PMI in the euro zone was 45.1%, which was a 1.1 percentage point increase from the previous month. In the core European countries, the manufacturing PMIs of Germany, the United Kingdom, and France were 44.7%, 49.5%, and 46.0%, respectively. Although they both recovered slightly, they remained below the 50% threshold. Affected by the weak demand, the prices of the main varieties of steel in the UK market continued to fall this month.

(3) Asian markets At the end of August, the CRU Asian steel price index was 182.6, down by 7.8 points month-on-month, down by 4.1%. Affected by the decline in exports and industrial output, Japan’s Manufacturing Purchasing Managers’ Index (PMI) fell to 47.7% in August, down 0.2% from the previous month, and below 50% for the third consecutive month, which was 16 months ago. The lowest level; the new export order index was 45.5%, the fifth consecutive month was below 50%, and the output sub-index fell to 46.9%, the lowest level since last April. Among other major economies in Asia, China's manufacturing PMI was 49.2%, a decrease of 0.9 percentage points from the previous month, and the fourth consecutive month of decline; the South Korean PMI was 47.5%, which was lower than 50% for the third consecutive month; India and China Taiwan's PMI dropped to 52.8% and 46.1%, respectively, which is the lowest level this year. The growth rate of the manufacturing industry in the major economies slowed down, and the demand for steel products was weak. The prices of major steel products in the Far East continued to fall this month, and the decline was larger than last month.

IV. Analysis of late-stage steel market price trends Affected by sluggish domestic and international market demand, both steel production and exports have shown a downward trend, the price reduction of raw materials has increased, and the social inventory has continued to decrease. The country has recently increased measures for steady growth. It is expected that the market will improve in the later period, and steel prices should show a steady state trend.

1. The state has stepped up its efforts in infrastructure construction to stimulate the growth of steel demand. This year, due to factors such as domestic adjustment of economic structure, changes in the mode of development, and the economic recession in the euro zone and the slowdown in the U.S. economic recovery, the demand for steel in international and domestic markets has increased. Obviously fall back. At the beginning of September in a speech at the APEC summit, the National Security Council pointed out that China will strengthen infrastructure construction and create a fair, transparent, and efficient political, legal, and market environment, and use infrastructure to stimulate domestic demand. Increase the employment and other positive aspects. At the same time, we must also increase the level of infrastructure in areas such as agriculture, energy, water conservancy, and information, and promote the construction of transportation networks such as railways, highways, waterways, civil aviation, and pipelines. Recently, the state has successively introduced a series of “steady-growth†policies, successively approved plans for rail transit construction in multiple cities across the country involving 25 projects, approved 13 regional highway projects, approved 10 environmental protection investment projects, and approved several airports. In the project and hydropower construction projects, it is expected that the weak market steel demand will improve in the later period.

2. Decline in increase in iron and steel production and supply restraint According to data from the National Bureau of Statistics, in the first eight months of this year, the accumulated investment in the fixed assets of the national steel industry was 417.3 billion yuan, an increase of 11.2% year-on-year, and the increase rate was 7.5 percentage points lower than the same period of last year. The investment in black smelting and rolling industry reached 322.5 billion yuan, a year-on-year increase of 7.7%, an increase of 10.6% from the same period of last year (see the table below), and the cumulative production of crude steel in China reached 48.157 million tons, an increase of 2.3% over the same period of last year. Compared with the same period last year, it dropped 8.3%. The average daily production level of crude steel in August was 1.893 million tons, a decrease of 4.84% compared with the previous period, and the supply of resources was significantly reduced. The oversupply of the steel market will be eased.

3. Decrease in prices of raw materials and weakened support to steel prices According to data from the National Bureau of Statistics, in August, the purchase price of industrial producers nationwide fell by 0.5% month-on-month and fell for the fourth consecutive month. The price of fuel and power dropped by 0.8%, and according to customs statistics, the average landed price of imported iron ore in August was US$129.83/ton, which was a decrease of US$4.97/ton from the previous period, a decrease of 3.69%, which was larger than that of the previous month. 0.62 percentage points; at the end of August, the prices of domestic fine iron powder, coking coal and metallurgical coke dropped by 7.46%, 10.88% and 13.90%, respectively, which increased by 2.76, 5.88 and 1.65 percentage points respectively from the previous month; the scrap price dropped by 4.34%. The price reduction of raw materials has increased, and the supporting effect on steel prices has further weakened.

The main issues that the market needs to pay attention to in the later period:

First, the price of some steel products has fallen below the cost of manufacturing, which has had a serious impact on corporate profits. After nearly four months of continuous decline, prices of rebar, wire rods, angle steel, medium plate, hot coil, and cold plate in the domestic market are already lower than the industry's manufacturing cost, which has brought serious impact on the economic benefits of iron and steel enterprises. . In the face of severe market conditions, steel companies should further control output, optimize product mix, and stabilize the market.

Second, iron and steel enterprises should further compress steel stocks and strictly control accounts receivable. From the statistics of large and medium-sized steel enterprises, the company’s steel inventories and accounts receivable all showed a rising trend, which not only affected the stability of the steel market, but also increased the company’s operating risks. The iron and steel enterprises must adhere to the operating principles of no contract, no production, no money, no delivery.

Third, there is still room for further decline in the price of imported iron ore. At the end of August, the CSPI domestic steel price index of the iron and steel institute has fallen back to the level of 2009, while in 2009 China's average imported iron ore cif price was US$80/ton, compared to the China Iron Ore Price Index (CIPOP) at the end of August. The average price of imported iron ore is 112.58 U.S. dollars per ton, but there is still much room for decline.